This is Part II of my article titled “Offering Memorandum Exemption Finally Proposed in Ontario! Other Regulators Also Mulling Changes. ” This article discusses some of the issues and concerns about the proposed changes to the OM Exemption contemplated by certain Canadian securities regulators. Capitalized terms not otherwise defined in this article have been defined in Part I of this article.

IV. Issues and concerns about the proposed changes to the OM Exemption

While the proposals are a positive step forward strongly supported by many capital markets participants across Canada, they do also give rise to a number of issues and concerns that industry and the Canadian securities regulator must work through during this public comment period. Some of the concerns are discussed below:

(a) Lack of a nationalized and harmonized OM Exemption

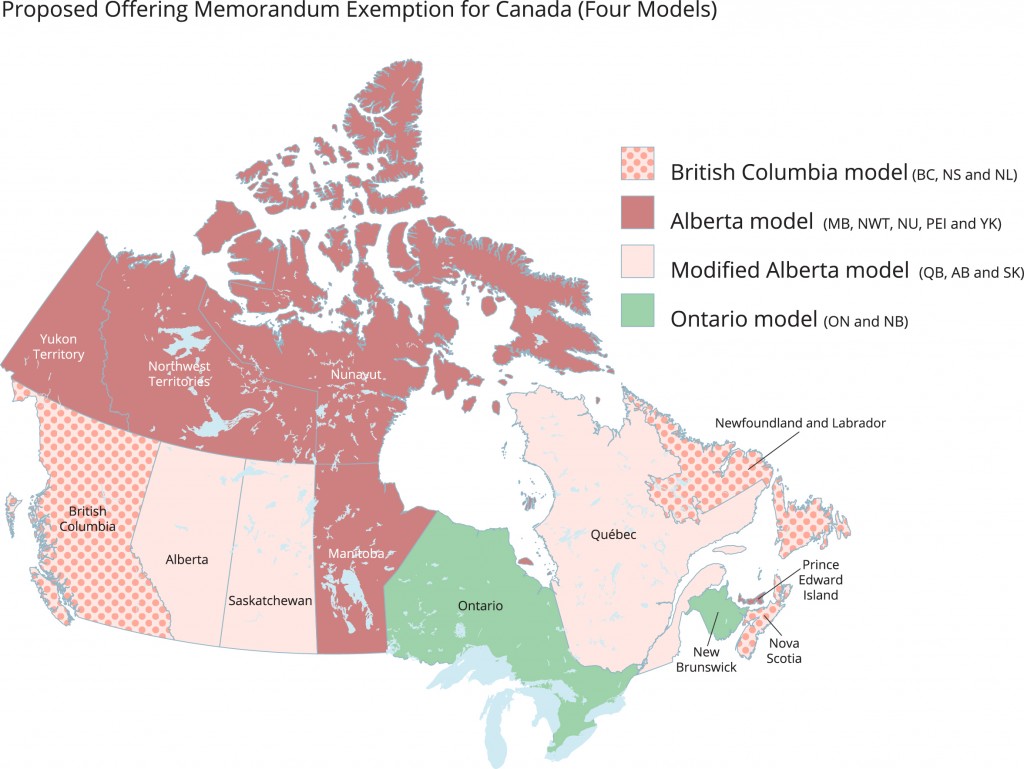

If all proposed changes are adopted by the various Canadian securities regulators, we would move from two to four models of the OM Exemption across Canada. This is moving us even further from a national or harmonized approach and reflects the increasing complexity of having 13 securities regulators across Canada. The significant challenges issuers and dealers will face in complying with this fractured approach to the OM Exemption is illustrated by the graphic below. This highlights which jurisdictions in Canada would follow which of the four models of the OM Exemption, assuming they are adopted as currently proposed.

(b) Prohibition on investment funds using the OM Exemption

It is not clear why the OSC has proposed excluding investment funds from the Ontario model of the OM Exemption and a clearer rationale is needed to support this exclusion. Whether an issuer is an investment fund or corporate issuer, arguably this does not matter, since the OM Exemption needs to be discussed at the same time and in the same forum. Allowing the Investment Funds Branch at the OSC deal with the OM Exemption by itself disconnects them from the many important policy and other discussions that are happening in the Corporate Finance Branch and in the various OSC Committees that have been established to provide the OSC with feedback, such as the OSC’s Exempt Market Advisory Committee.

(c) Prohibition on proprietary products of related issuers

It is not clear why an issuer who seeks to rely on the OM Exemption should be precluded from doing so through a related dealer firm. The prohibition suggest the CSA believes there are conflicts of interest so insurmountable that appropriate ’know-your-product’, ‘know-your-client’ and suitability assessments are not possible by a related dealer. It should be noted that significant participants in the mutual fund dealer and investment dealer communities regularly, and often exclusively, sell proprietary products or securities of related issuers. Surely the conflict mitigation approaches employed by those sectors of the capital markets under applicable securities law should be available to all registered dealers. An outright prohibition appears unjustified and disproportional absent further explanation from the CSA.

The impact of the related party prohibition would be significant for multiple issuer groups including mortgage investment corporations, real estate and oil and gas companies that have in-house registered dealers who would be unable to sell securities of their own issuers to Ontario investors under the proposed Ontario model of the OM Exemption.

(d) $30,000 investment limit per year

The introduction of investment limits on eligible investors for trades through a registered dealer is unsatisfactorily explained. Registered dealers have suitability obligations under applicable securities law and should be allowed the professional discretion to evaluate the suitability of any amount an investor may choose to invest. The sale of investments that are unsuitable for a client by their nature, or because of the size of the investment, are well within the existing jurisdiction of the CSA to investigate and pursue regulatory action against the firm if warranted.

For example, for an investor with $800,000 of net assets (and who does not satisfy any of the financial tests for qualifying as an accredited investor) investing in more than $30,000 of exempt market securities may be very suitable. For others, an investment of even $30,000 may be totally unsuitable. That is why the suitability rule exists and arguably there is no need for an investment limit. The CSA need to trust registered dealers to do their job and have faith in the securities regulatory framework that they have developed or provide more education through outreach programs or regulatory guidance explaining how suitability is to be done in a compliant manner.

In addition to the above, the amount of the proposed limit also raises questions. We know the Alberta Securities Commission’s (the ASC) review of the OM Exemption in Alberta for 2011 and 2012 indicated that the average size of an investment by an individual eligible investor was $45,700 in 2011 and $47,900 in 2012 while the median was approximately $26,200 and $27,500 respectively. It would appear that the proposed $30,000 investment limit for eligible investors was based on the median investment size rather than the average investment size. Such data, if indeed the source of the proposed limit, is only based on two years and reflects the experience of only a single CSA member. Furthermore, the CSA has not provided any evidence to indicate that the proposed investment limits, if implemented, would not negatively impact the amount of capital raised or lead to circumstances when an investment by an eligible investor may well have been a suitable investment.

(e) Excluding principal residence from the net asset test for eligible investors

Only Ontario is proposing to exclude the value of a principal residence from the net asset test for eligible investors. The OSC has not provided supporting arguments for this change although Alberta, Quebec and Saskatchewan have proposed conducting further research and analysis in respect of the implications of excluding the principal residence.

Summary

The Ontario model and proposed changes to the OM Exemption by the Participating Jurisdictions are a cause for excitement but also a measure of concern in the private capital markets. The occasion of Ontario’s entry into the OM Exemption should be a time for celebration, yet we still find ourselves unsure about the disconnected approach to these fundamental capital raising tools from one end of the country to the other.

Thankfully, the restrictions discussed above are only at the proposal stage. Capital markets participants have an opportunity to continue working with the OSC and other CSA members in the Participating Jurisdictions to ensure that the adoption of the OM Exemption in Ontario actually has the potential to increase access to capital and the economic development and job creation that comes with it.

The OSC is accepting comments on their proposed OM model of the OM Exemption and other capital raising exemptions they are considering until June 18. 2014. Your comments and views are important and you are strongly encouraged to submit a comment letter.

* * *

Disclaimer

This blog is not intended to create, and does not create an attorney-client relationship. You should not act or rely on information on this blog post without first seeking the advice of a lawyer. This material is intended for general information purposes only and does not constitute legal advice. For legal issues that arise, the reader should consult legal counsel.

Brian Koscak is a Partner at Cassels Brock & Blackwell LLP located in Toronto, Ontario and Chair of the Private Capital Markets Association of Canada (formerly, the Exempt Market Dealers Association of Canada). Brian is also a member of the Ontario Securities Commission’s Exempt Market Advisory Committee and Co-Chair of the Equity Crowdfunding Alliance of Canada. Brian can be reached by phone at 416-860-2955, by e-mail at bkoscak@casselsbrock.com or on twitter @briankoscak. Brian also regularly writes about Canadian securities law matters on his personal blog at www.briankoscak.com.

Brian Koscak is a Partner at Cassels Brock & Blackwell LLP located in Toronto, Ontario and Chair of the Private Capital Markets Association of Canada (formerly, the Exempt Market Dealers Association of Canada). Brian is also a member of the Ontario Securities Commission’s Exempt Market Advisory Committee and Co-Chair of the Equity Crowdfunding Alliance of Canada. Brian can be reached by phone at 416-860-2955, by e-mail at bkoscak@casselsbrock.com or on twitter @briankoscak. Brian also regularly writes about Canadian securities law matters on his personal blog at www.briankoscak.com.

[…] The “OM Exemption” refers to the offering memorandum prospectus exemption set out in Section 2.9 of National Instrument 45-106 – Prospectus and Registration Exemptions. You can read a prior article that explains the OM Exemption in a here and some of the issues and concerns involving the OSC’s proposed changes to the OM Exemption here. […]