On March 20, 2014, the Ontario Securities Commission (the OSC) published for comment a long awaited proposal for a new offering memorandum exemption in Ontario based on a variant of the Alberta model as set out in Section 2.9 of National Instrument 45-106 Prospectus and Registration Exemptions (the OM Exemption). On the same date, Canadian securities regulators in Alberta, Quebec, Saskatchewan and New Brunswick also published for comment proposed amendments to their respective OM Exemptions.

Part I of this article provides a basic primer on the OM Exemption, Part II discusses the proposed Ontario OM model and Part III discusses the proposed amendments to the Alberta model contemplated by Alberta, Quebec and Saskatchewan (the “Participating Jurisdictions”) while New Brunswick is proposing to align with the new Ontario model. Part IV of this article discusses some of the issues and concerns that capital markets participants may have in connection with these complex and inter-related changes to the OM Exemption across the jurisdictions.

I. The Offering Memorandum Exemption – A Basic Primer

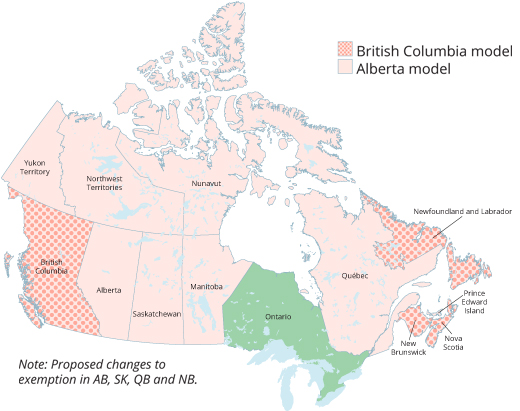

There are two existing models of the OM Exemption in Canada: the ‘British Columbia model’ and the ‘Alberta model’. The British Columbia model is currently in effect in the Provinces of British Columbia, New Brunswick, Nova Scotia and Newfoundland and Labrador. The Alberta model is currently in effect in the Provinces of Alberta, Manitoba, Prince Edward Island, Québec, Saskatchewan and the Northwest Territories, Nunavut and the Yukon. Ontario does not currently have an OM Exemption but is considering implementing a variant of the Alberta model.

The graphic below set out the availability of the OM Exemption and different models across Canada today.

Under both of these existing models, a purchaser buys a security as principal and at the same time, or before the purchaser signs the purchase agreement, the issuer:

(a) delivers a prescribed form of offering memorandum (OM) to the purchaser;

(b) obtains a signed risk acknowledgement form from the purchaser; and

(c) satisfies other requirements (as discussed below).

Under both models, issuers can sell securities to the public with no limit on the amount of capital that can be raised by an issuer or the amount invested by an investor. The key difference is that under the Alberta model any investor who does not qualify as an “eligible investor” is limited to a maximum of $10,000, while “eligible investors” have no investment limits.

An “eligible investor” is a person who has:

(a) net assets, alone or with a spouse, in the case of an individual, that exceed $400,000;

(b) net income before taxes that exceeded $75,000 in each of the two most recent calendar years and who reasonably expects to exceed that income level in the current calendar year; or

(c) net income before taxes, alone or with a spouse, in the case of an individual, that exceeded $125,000 in each of the two most recent calendar years and who reasonably expects to exceed that income level in the current calendar year.

Generally, reliance on the OM Exemption requires satisfying the following requirements:

(a) Commission and finder’s fee – no commission or finder’s fee may be paid to any person, other than a registered dealer, in connection with a distribution to a purchaser in the Northwest Territories, Nunavut or the Yukon. It is permitted in the other jurisdictions.

(b) Prescribed form of OM – an OM must be in compliance with the prescribed form requirements, as set out in Form 45-106 F2 – Offering Memorandum for Non-Qualifying Issuers, which describes the form requirements for private issuers. There is a separate form for public issuers.

(c) Audited financial statements – issuers are required to include audited financial statements and interim financial statements for the most recently completed interim period that ended more than 60 days before the date of the OM, subject to a number of requirements.

(d) Cancellation right and holding funds in trust – an OM must provide the purchaser with a contractual right to cancel the agreement to purchase the security (if the securities legislation where the purchaser is resident does not provide a comparable right) by delivering a notice to the issuer not later than midnight on the second business day after the purchaser signs the agreement to purchase the security. Accordingly, the issuer must: (a) hold in trust all consideration received from the purchaser in connection with a distribution of a security until midnight on the second business day after the purchaser signs the agreement to purchase the security; and (b) return all consideration to the purchaser promptly if the purchaser exercises the right to cancel the agreement to purchase the security.

(e) Statutory rights of action – the OM must contain a prescribed contractual right of action against the issuer for rescission or damages if the securities legislation where the purchaser is resident does not provide a statutory right of action in the event of a misrepresentation in an OM delivered to a purchaser.

(f) Certificate – the OM must contain a certificate page that states the OM does not contain a misrepresentation which must be signed by individuals holding certain titles within an issuer, which varies depending on the type of legal entity that is offering the securities. This certificate must be true at the date the certificate is signed and delivered to a purchaser. If a certificate ceases to be true after it is delivered to a purchaser, the issuer cannot accept an agreement to purchase the security from a purchaser unless: (a) the purchaser receives an updated OM; (b) the updated OM contains a newly dated and signed certificate; and (c) the purchaser resigns the agreement to purchase the security.

(g) Risk acknowledgement form – an investors risk acknowledgement form must be in the required form and an issuer relying on it must retain the signed document for eight years after the distribution.

(h) Filing the OM and any updated OM – the issuer must file a copy of an OM delivered to a purchaser and any update of a previously filed OM with the local securities regulatory authority on or before the 10th day after the distribution of the OM or updated OM.

II. Big Step Forward in Capital Raising in Ontario – OSC Proposes a Form of OM Exemption

Finally, after many years of lobbying by various capital markets participants, the OSC has announced a significant step forward by proposing to adopt a form of the OM Exemption in Ontario. Many industry voices believe that adopting the OM Exemption in Ontario will noticeably improve capital raising opportunities at a time when many issuers are struggling to raise capital – particularly in Ontario.

Under the proposed Ontario form of OM Exemption (the Ontario model), the OSC is proposing to adopt the Alberta model with the following modifications:

(a) changing the definition of “eligible investor” and introducing investment limits for all investors (see below);

(b) excluding novel and complex products, such as specified derivatives and structured finance products;

(c) prohibiting registrants that are related to an issuer from participating as a dealer in a distribution; and

(d) imposing limited ongoing continuous disclosure requirements on private non-reporting issuers including:

-

the delivery of audited financial statements within 120 days after the end of a non-reporting issuer’s financial year, in addition to a notice on the use of the aggregate proceeds raised in all distributions involving the OM Exemption in accordance with the audit requirements for reporting issuers; and

-

an ‘event notice’ upon the occurrence of certain specified events.

Under the Ontario model, the OSC proposes that:

(a) if the purchaser is an “eligible investor”, they are limited to investing $30,000 in the preceding 12-months, unless the person is also qualified as an “accredited investor”; if the investor is not an “eligible investor” then they will be limited to $10,000 in the preceding 12-months;

(b) the definition of “eligible investor” be amended to:

- exclude an individual’s primary residence;

- remove the “net income” test for non-individuals (e.g., companies);

- reduce the net asset test for individuals from $400,000 to $250,000 (having removed the principal residence for the calculation) and for non-individual investors, the net asset test would remain at $400,000.

To make things a little more complicated, as Ontario proposes to implement a modified Alberta model, there is now a movement led by Alberta, to change the Alberta model OM Exemption.

III. Alberta also making Proposed Changes to the Offering Memorandum Exemption

At the same time as Ontario published the Ontario model for comment, Alberta, Quebec and Saskatchewan have also proposed further amendments to the OM Exemption (the Modified Alberta model), including changes which would:

(a) impose investment limits on eligible investors such that the acquisition cost to a purchaser:

- who is an individual cannot exceed $30,000 in the preceding 12-months except a purchaser who is an accredited investor or person in s. 2.5(1) of NI 45-106 [family, friends and business associates]; or

- $10,000 if a non-eligible investor in the preceding 12-months.

(b) investments by non-eligible investors would be limited to no more than $10,000 in a 12-month period and not per distribution.

If adopted, Alberta, Quebec and Saskatchewan would be moving from the Alberta model to this new Modified Alberta model.

Part II will posted in my next blog which discusses Issues and concerns about the proposed changes to the OM Exemption

* * *

Disclaimer

This blog is not intended to create, and does not create an attorney-client relationship. You should not act or rely on information on this blog post without first seeking the advice of a lawyer. This material is intended for general information purposes only and does not constitute legal advice. For legal issues that arise, the reader should consult legal counsel.

Brian Koscak is a Partner at Cassels Brock & Blackwell LLP located in Toronto, Ontario and Chair of the Private Capital Markets Association of Canada (formerly the Exempt Market Dealers Association of Canada). Brian is also a member of the Ontario Securities Commission’s Exempt Market Advisory Committee and Co-Chair of the Equity Crowdfunding Alliance of Canada. Brian can be reached by phone at 416-860-2955, by e-mail at bkoscak@casselsbrock.com or on twitter @briankoscak. Brian also regularly writes about Canadian securities law matters on his personal blog at www.briankoscak.com.

Brian Koscak is a Partner at Cassels Brock & Blackwell LLP located in Toronto, Ontario and Chair of the Private Capital Markets Association of Canada (formerly the Exempt Market Dealers Association of Canada). Brian is also a member of the Ontario Securities Commission’s Exempt Market Advisory Committee and Co-Chair of the Equity Crowdfunding Alliance of Canada. Brian can be reached by phone at 416-860-2955, by e-mail at bkoscak@casselsbrock.com or on twitter @briankoscak. Brian also regularly writes about Canadian securities law matters on his personal blog at www.briankoscak.com.

[…] and Registration Exemptions. You can read a prior article that explains the OM Exemption in a here and some of the issues and concerns involving the OSC’s proposed changes to the OM Exemption […]